Banking Beyond the Branch

How Pebuu builds the human infrastructure of financial inclusion

How Pebuu builds the human infrastructure of financial inclusion

Watch: The Impact Entrepreneur Breakthrough, presented

Peace needs an accounting standard, not another argument

Lebanon’s survival economy shows the limits of dollarization without recovery

What mission-driven founders need to know before converting

How three Skoll Awardees build public systems for lasting impact

Thirty percent of Americans lack access to affordable banking services that can support them during difficult times. Unfortunately, the pandemic exacerbated this reality and the latest economic challenges only worsen the matter. Those who lost jobs during the pandemic became further unprepared for financial emergencies. Among laid-off workers, minorities, in particular, faced great financial management hurdles. Getting a loan when needed, such as buying a car or home, is impossible for many. According to the Consumer Finance Protection Bureau (CFPB), 1 out of 5 adults are “credit invisible” and hence ineligible for a loan, despite many who make regular rent or utility payments.

According to the Fed, almost half of credit applicants in 2021 with income below $50,000 were rejected or received less than what they applied for, compared with only 13 percent of those with income above $100,000. No file or thin file consumers are not necessarily riskier than thick credit file consumers. There is a plethora of data available that lenders need to get better at accessing and leveraging to determine risk profiles and credit worthiness.

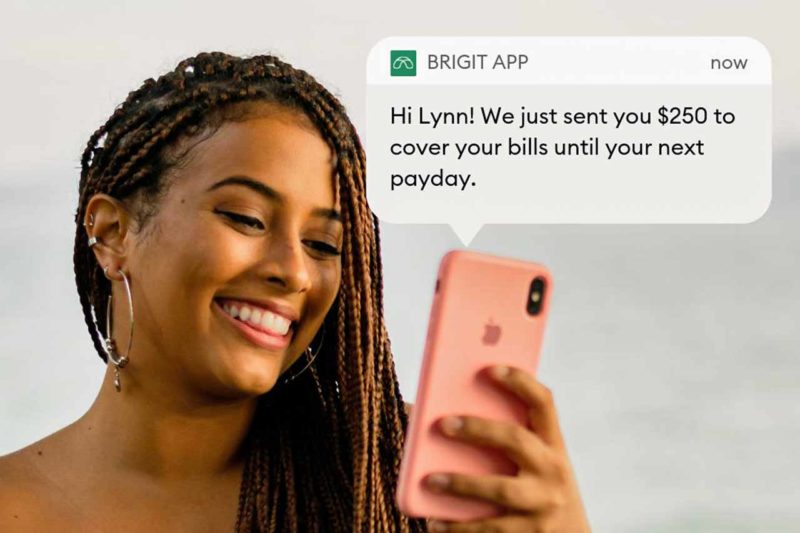

For decades, banks, credit unions, and community development finance institutions (CDFIs) have offered services to help people build credit. Today, a growing number of fintech startups are leveraging efficiencies driven by technology to address credit inequities. Brigit, a NY-based Fintech, is on a mission to reduce the daunting burden of overdraft fees and help people build strong credit scores. Considering that the CFPB reports annual overdraft fees at roughly $15b and disproportionately affect the least wealthy consumers, Brigit’s mission is worthwhile.

Hamel Kothari, Brigit’s CTO and Co-Founder, launched Brigit because he saw family members struggling with financial stress. Brigit offers advances to pay bills and credit builder loans for a monthly subscription, boasting hundreds of thousands of paying customers. Users connect their bank account allowing Brigit’s algorithms to analyze cash flow data, determine financial needs and loan eligibility, and provide money management services. These include Alerts to notify if someone is at risk of account overdraft and offer automated advances to avoid fees. As a result, Brigit’s users have been saving an average of $344 on overdraft fees annually and 45% of customers claim they’re now able to avoid using exploitative payday loans.

Brigit’s Credit Builder product allows people to apply for a loan to improve their credit score. The loan is interest free, setting Brigit apart from predatory ‘payday lenders’. Loan funds are held at Brigit’s partner bank and secured until payments are made. Borrowers make repayments and, once the loan is paid off, those funds are returned to the borrower. Repayments are automatically reported to credit bureaus, demonstrating the borrower's loan repayment behavior, contributing to their credit score.

Nearly 106 million U.S. consumers are unable to secure credit at mainstream rates either because they’re credit invisible or lack a credit score that typically enables access.

Brigit also offers a free version providing tools like budgeting, bill forecasting, and alerts. Hamel shared that, from a survey of Brigit’s customers, 94% felt Brigit helped them achieve financial goals, 59% avoided overdraft fees, 45% didn’t need payday loans and 79% cited mental health improvement. Helping understand spending habits and get a handle on bills is what many Americans need to improve their financial health.

Gaining a money management and cash flow picture of a loan applicant, in addition to credit scores, is critical to determine loan eligibility. But how is this possible when many financial transactions go unreported? According to Experian, nearly 106 million U.S. consumers are unable to secure credit at mainstream rates either because they’re credit invisible or lack a credit score that typically enables access. Research shows that by using expanded data sets, such as rental payments, utility information and more, lenders can improve access to credit for nearly 50 million credit invisible consumers.

Fintech companies, like Esusu, address this challenge by leveraging the immense value in rent transactions. NY-based Esusu built a platform that automates the reporting of on-time rental payments to the three major credit bureaus, potentially increasing a borrower's credit score. In the U.S. there are 44m renting households comprising about 80m individuals and less than 10% of these rent payments are reported to credit bureaus. Furthermore, credit scores are on average 100 points lower for renters than mortgage payers, with minorities disproportionately affected. Making regular, on-time rent payments demonstrates capacity to pay and good character, attributes showing you’re a responsible consumer.

Esusu’s customers comprise a vast range of property managers and housing providers that connect their property management software to Esusu’s platform via API. This allows property managers to monitor rental payments and automatically report on-time payments to credit bureaus. Alexis Sofyanos, Esusu’s VP Revenue & Business Development, claims they’ve helped renters increase credit scores on average by 35 points and establish tens of thousands of first-time scores. For housing providers, rent payment reporting is fully automated providing an important benefit to tenants. In turn, they not only see an increase in on-time payments but a growing set of financially stable tenants.

People with lower credit scores pay higher APRs on loans reducing their cash flow for daily needs, perpetuating a low-income lifestyle.

To further social impact, Esusu offers a reporting service helping property managers and investors understand and report their social impact metrics. Thus far, Esusu has helped over 1 million renters across the U.S. For many Americans, rental payments are the main financial transaction in their lives. Reporting these transactions can stabilize and increase a credit score and over time open up new economic opportunities, such as qualifying for an affordable loan or even a job. People with lower credit scores pay higher APRs on loans reducing their cash flow for daily needs, perpetuating a low-income lifestyle.

It’s difficult enough to build a good credit score but millions of U.S. immigrants arrive without any credit identity, excluding them from everyday financial services — finding a home or even getting a mobile phone can prove impossible. Yet many immigrants have credit history in their country of origin, valuable data that provides insights into credit worthiness. Nova Credit, a U.S. fintech founded by impact entrepreneur and immigrant Misha Esipov in 2016, assembles this international data helping immigrants gain access to U.S. credit.

It’s difficult enough to build a good credit score but millions of U.S. immigrants arrive without any credit identity, excluding them from everyday financial services — finding a home or even getting a mobile phone can prove impossible. Yet many immigrants have credit history in their country of origin, valuable data that provides insights into credit worthiness. Nova Credit, a U.S. fintech founded by impact entrepreneur and immigrant Misha Esipov in 2016, assembles this international data helping immigrants gain access to U.S. credit.

Nova Credit helps individuals improve their financial health and financial institutions serve a wider set of customers, especially the underserved. Nova Credit solves this info asymmetry challenge by working with international credit bureaus, compiling and reviewing data, checking compliance requirements, and deploying a methodology to translate and level-set attributes to create consumer-permissioned credit scores for U.S. lenders — the Credit Passport. Real-time integration with 20 countries allows Nova Credit to access 1+ billion consumer records globally. Credit Passport is used by dozens of Nova Credit’s customers including lenders like HSBC (also an investor), American Express, Verizon, and student lenders like mPower and Prodigy. Applicants check a box on the application confirming they have credit history in a different country. Credit Passport enables consumers to paint a complete picture of their financial identity and allows businesses to lend more fairly and responsibly. American Express claims that accounts approved using Credit Passport are 75% less risky than domestic account holders with prime credit scores.

During the pandemic, Nova Credit explored another banking challenge: consumer loan rejections due to limited data. Bank accounts include many cash flow transactions that can be used to determine credit worthiness (income, expenses, etc.). To enable lenders with risk assessment, Nova Credit developed Cash Atlas, which pulls transactional data from bank accounts and digitally provides it to lenders. This additional data provides valuable insights into liquidity, transactional activity, and affordability of mainstream consumers, especially helping low-no-file applicants. This new product is helping several banks better predict risk and gain a complete picture on applicants. Esipov states they engage over a million newcomers annually and approximates that customers have experienced loan approval rates in the 50-60% range.

Together, these and other impact entrepreneurs run Fintech companies across the U.S. that aim to solve inequities and improve the financial health of millions of Americans.

Related Content

How Pebuu builds the human infrastructure of financial inclusion

Watch: The Impact Entrepreneur Breakthrough, presented

Peace needs an accounting standard, not another argument

How self-directed IRAs can open a path to impact investing

Comments

Deep Dives

RECENT

Editor's Picks

Webinars

News & Events

For AI governance, strategic foresight, digital economy policy, and institutional design.

Helps foundations, DAF holders, and family offices model how impact-first investing can extend charitable capital

Subscribe to our newsletter to receive updates about new Magazine content and upcoming webinars, deep dives, and events.

Become a Premium Member to access the full library of webinars and deep dives, exclusive membership portal, member directory, message board, and curated live chats.

0 Comments