“I Didn’t Know My DAF Could Do This!”

How donor-advised funds are becoming catalytic capital platforms

How donor-advised funds are becoming catalytic capital platforms

Why circular migration may offer a better path than mass repatriation

Financing historic cities for housing, livelihoods, and resilience

How Haverford’s student investing program pivoted toward more purpose-suited capital

Abrupt UK cuts threaten coastal resilience, food security, and community-led adaptation

At MIE 2026, investors reframed risk as a tool for scale, resilience, and courage

Limited access to affordable financial services for many Americans is deepening the wealth divide across the U.S. According to the Federal Reserve, 40% of American adults wouldn’t be able to cover a $400 emergency with cash, savings, or a credit-card charge that they could quickly pay off. Unfortunately, the pandemic exacerbated this reality, and a segment of the American population has been hit brutally hard. 30% of Americans lack access to affordable banking services that can support them during difficult times and 59 million Americans use government benefits just to get by financially.

Almost half of US credit applicants in 2021 with income below $50,000 were rejected or received much less than what they applied for. So, without access to credit and limited savings, these difficulties not only affect individuals but the economy at large. Having emergency savings plays a significant role in family financial stability. Furthermore, if you don’t have money in the bank to withstand a financial emergency, your ability to maintain long term goals is severely impacted. According to a report by the Pew Research Center, around half of adults in the U.S. said that their finances were negatively affected by the pandemic, and around a quarter said that they had trouble paying their bills.

Photo Courtesy of Maddie McGarvey

Photo Courtesy of Maddie McGarvey

Fortunately, there’s a growing batch of impact entrepreneurs running fintech companies that help people better manage their financial lives and improve their financial health.

Courtesy of SaverLife

Courtesy of SaverLife

Even if eligible, not everyone should take a loan. Building savings can be a stable, attractive alternative to building financial health and managing financial emergencies. Yet developing consistent saving behavior has been difficult for millions of Americans struggling to make ends meet. Saverlife, a national non-profit Fintech, has been driving this behavior change for the past 20 years by offering a platform that incentivizes people to save regularly. People sign up, become members, attach their savings account, pre-paid account, or PayPal and become eligible for weekly cash awards and giveaways. Saverlife’s mission is to foster regular savings habits which in turn builds resilience and financial stability.

Saverlife, via an API, reviews account activity of its members and awards progress and achievement of defined savings goals. Consistent weekly cash prizes prove to be a significant motivation to their 600K members spread across 50 states from low-income households. The median income of a SaverLife member is between $25,000-$35,000, and two-thirds of new members link an account with a savings balance of less than $100.

Using SaverLife, over 60% of members make regular monthly savings contributions and over 30% save as much as $100 per month. CEO Leigh Phillips, reports Saverlife’s impressive social impact record reaching over 80% women members, many mothers and hourly workers with highly inconsistent earnings and volatile expenses. The incentives seem to be impactful — member accounts show savings balances increase 3x after only 6 months of membership. Furthermore, according to a 2020 study, having a savings balance above $100 is correlated with avoiding high-cost borrowing and being more likely to keep utilities switched on.

The behavior change is partially driven by Saverlife’s financial education offerings. Members earn points as they learn about money management and could win cash prizes — already receiving over $4.5m USD in rewards. In addition to the engaging campaigns and chance to win cash, Saverlife offers community forums with relatable stories, education on how to claim benefits and referrals for various services — members have a lot of help at their fingertips to improve their financial health and increase their overall well-being.

Having emergency savings plays a significant role in family financial stability.

With financing from corporate, foundation, and individual philanthropy, Saverlife offers all of these services for free to low-income Americans. Recently, they began offering a customizable version of the platform to enterprise clients such as employers, nonprofits, and credit unions, a fee-for-service model, which will eventually help to sustainably fuel growth and support millions more Americans.

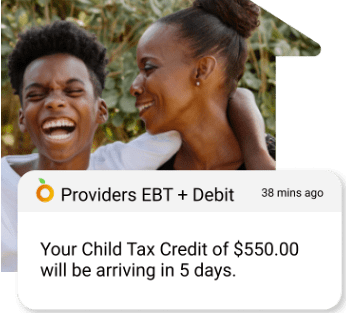

Digital tools drive convenient access to these types of financial services, but how do you manage money or a financial emergency if you aren’t eligible for credit and have limited income to save? Fortunately, there’s a range of government benefits that help low-income Americans. These services have existed for years but lack the much-needed ease and convenience required by participants. Impact entrepreneur Jimmy Chen, Founder & CEO of Propel, understood these usage pain points and launched a digital platform in 2014 to help Americans better manage their benefits and money.

Courtesy of Propel

Courtesy of Propel

Using Providers, Propel’s mobile app, participants can digitally manage their benefits such as the U.S. Supplemental Nutrition Assistance Program (SNAP) or the Women, Infants, & Children benefit (WIC). To spend these funds, participants must use a government issued Electronic Benefit Transfer card, which operates like a debit card along with a 1-800 number. However, using the Providers app, the account is digitized so now users can see their account balance before going shopping, make appropriate spending decisions, and get notified when government benefits hit their account. This builds confidence when people know they have funds to buy food or when the next credit will arrive to feed their family. Being able to manage benefit funding allows participants to optimize their money and ensure food security for their family. Today, Propel helps over 5 million low-income Americans, 80% of which are parents with at least one child living at home to support. A study by Harvard economists showed that using Providers helped stretch SNAP food benefits by an average of two days per month.

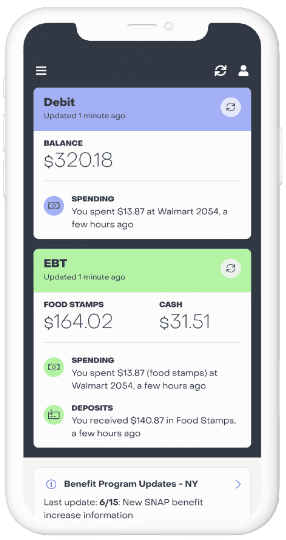

Providers also offer a debit card so users can better manage their money. Users rely on this card as a direct deposit source for incoming funds including cash-based government benefits, like tax credits and disability, because the card doesn't charge monthly or overdraft fees, and is integrated into an app that manages benefit accounts. Providing these types of mobile banking services also allows Propel to analyze account activity and further educate people about the full set of benefits that are available and for which they may qualify.

Courtesy of propel

Courtesy of propel

Jimmy’s vision is to address the full financial health of customers. Hence Providers acts like a digital distribution channel offering a wide range of benefits to low-income populations from many organizations that also serve this demographic. Besides mobile banking, users can also access a variety of money savings & money-making offers like local job postings, discounts for utilities, grocery coupons, and even receive philanthropic funding. Propel doesn’t charge for their services and earns revenues through merchant interchange fees and lead generation fees from 3rd party service partnerships. Propel closely monitors their social impact and the financial health of their customers, including surveying households to understand the impact from external factors like a changing economy, public health, and policy interventions. A recent survey for example, showed that 8.4% of Providers users reported being evicted or foreclosed upon in the past month, a 35% increase from September 2022. By understanding and designing services to address the current pain points of low-income Americans, the Providers app is working to help people better weather financial shocks they may experience.

Together, these and other impact entrepreneurs run Fintech companies across the U.S. aiming to solve the inequities and improve the financial health of millions of Americans.

Related Content

How donor-advised funds are becoming catalytic capital platforms

Why circular migration may offer a better path than mass repatriation

Financing historic cities for housing, livelihoods, and resilience

Democracy, narrative, and systems change

Comments

Deep Dives

RECENT

Editor's Picks

Webinars

News & Events

Helping founders and impact investors align

For three craft enterprises in India

Subscribe to our newsletter to receive updates about new Magazine content and upcoming webinars, deep dives, and events.

Become a Premium Member to access the full library of webinars and deep dives, exclusive membership portal, member directory, message board, and curated live chats.

Join our global community of systems-minded changemakers.

Subscribe to the Impact Entrepreneur newsletter for the latest insights, magazine features, and invitations to exclusive webinars, Deep Dives, and events.

0 Comments